The Community Reinvestment Act (CRA) was enacted in response to the devastating impact of redlining-a practice once used by banks to define communities of color and refuse them service. To this day neighborhoods have not recovered from this discrimination, such as this block in Niagara Falls where every home is condemned. The CRA is now the backbone of our work and our relationships with banks.

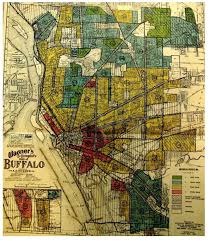

This 1937 federal underwriting map shows redlining at work. Most African Americans lived in the red zones.

Source: Residential Security Map, Buffalo, N.Y., City Survey File. Record Group 195. National Archives II, College Park MD. Image courtesy of Carl Nightingale

The Community Reinvestment Act (CRA) was enacted in 1977 in response to the devastating impact of discriminatory lending practices against communities of color and low-to-moderate income neighborhoods; a practice known as redlining.

Purpose?

The CRA has two purposes:

To redress the

impact of redlining.

To encourage banks to meet the credit needs of all segments of the communities in which they serve – including low – to – moderate income individuals and neighborhoods.

A new study shows, 3 out of 4 neighborhoods “redlined” on government maps 80 years ago continue to struggle today economically.” – Washington Post

Although the CRA was legislation put forth in direct response to redlining, the Act itself does not explicitly include race, but looks to see reinvestment in low-to-moderate (LMI) neighborhoods and individuals.

With it’s passing, the CRA created regulatory bodies to oversee that banks were compliant with the Act. These regulators assess each banks record in fulfilling its obligation to the community and use those records in evaluating bank applications for mergers.

The Regulators Who Evaluate Bank Performances Are:

And in NYS, the Department of Financial Services (DFS)

The CRA does NOT

Prescribe ratios or benchmarks for regulators to use during their exam, nor does it require banks to make high risk loans that jeopardize their financial stability. On the contrary, the law makes it clear a bank’s CRA activities must be consistent with the safe and sound operations of the bank.

The Coalition works within the framework of the CRA as the backbone of our work and the relationships we have cultivated with banks. Beyond this, BNCRC is deeply in touch with the racial aspect/angles/lens to traditional banking and fight to keep that at the center of this work as we build equity in our region.